VOLUME 1

xecutive summary

The energy transition is off-track. The aftermath of the COVID-19 pandemic and the ripple effects of the Ukraine crisis have further compounded the challenges facing the transition. The stakes could not be higher – every fraction of a degree in global temperature change can trigger significant and far-reaching consequences for natural systems, human societies and economies.

Limiting global warming to 1.5°C requires cutting carbon dioxide (CO₂) emissions by around 37 gigatonnes (Gt) from 2022 levels and achieving net-zero emissions in the energy sector by 2050. Despite some progress, significant gaps remain between the current deployment of energy transition technologies and the levels needed to achieve the goal of the Paris Agreement to limit global temperature rise to within 1.5°C of pre-industrial levels by the end of this century. A 1.5°C compatible pathway requires a wholescale transformation of the way societies consume and produce energy.

Current pledges and plans fall well short of IRENA’s 1.5°C pathway and will result in an emissions gap of 16 Gt in 2050. Nationally Determined Contributions (NDCs), long-term low greenhouse gas emission development strategies (LT-LEDS) and net-zero targets, if fully implemented, could reduce CO₂ emissions by 6% by 2030 and 56% by 2050, compared to 2022 levels. However, most climate pledges are yet to be translated into detailed national strategies and plans – implemented through policies and regulations – or supported with sufficient funding. According to IRENA’s Planned Energy Scenario, the energy-related emissions gap is projected to reach 34 Gt by 2050, underscoring the urgent need for comprehensive action to accelerate the transition.

Annual deployment of some 1 000 GW of renewable power is needed to stay on a 1.5°C pathway. In 2022, some 300 GW of renewables were added globally, accounting for 83% of new capacity compared to a 17% share combined for fossil fuel and nuclear additions. Both the volume and share of renewables need to grow substantially, which is both technically feasible and economically viable.

Policies and investments are not consistently moving in the right direction. While there were record renewable power capacity additions in 2022, the year also saw the highest levels of fossil fuel subsidies ever, as many governments sought to cushion the blow of high energy prices for consumers and businesses. Global investments across all energy transition technologies reached a record high of USD 1.3 trillion in 2022, yet fossil fuel capital investments were almost twice those of renewable energy investments. With renewables and energy efficiency best placed to meet climate commitments – as well as energy security and energy affordability objectives – governments need to redouble their efforts to ensure investments are on the right track.

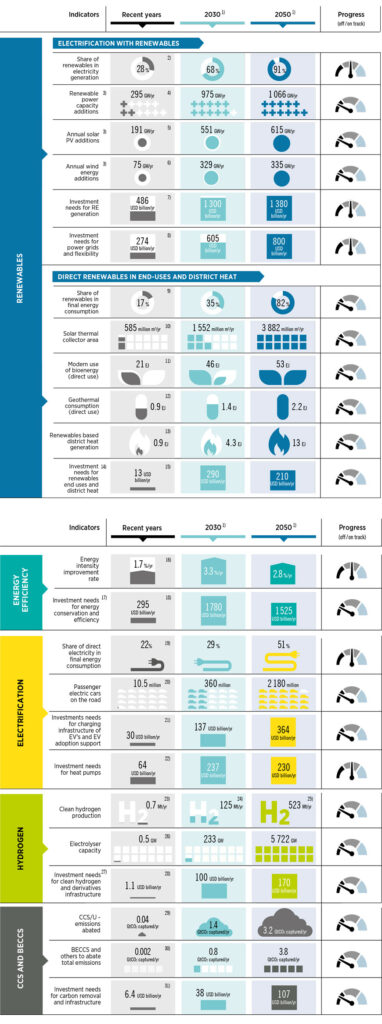

Every year, the gap between what is achieved and what is required continues to grow. IRENA’s energy transition indicators (Table S1) show significant acceleration is needed across energy sectors and technologies, from deeper end-use electrification of transport and heat, to direct renewable use, energy efficiency and infrastructure additions. Delays only add to the already considerable challenge of meeting IPCC-defined emission reduction levels in 2030 and 2050 for a 1.5°C trajectory (IPCC, 2022a). This lack of progress will also increase future investment needs and the costs of worsening climate change effects.

TABLE S1 Tracking progress of key energy system components to achieve the 1.5°C Scenario

Table S1 notes: [1] Average annual investments requirement to reach the 1.5°C target during the period 2023 – 2030 and 2023 – 2050 are shown in the investments rows under 2030 and 2050, respectively. All investment figures for recent years are in current USD; the particulars of recent years used for the indicators are: [2] 2020; [3] net capacity additions for 2030 and 2050 are excluding replacement stock for end-of-life units; [4] 2022; [5] 2022; [6] 2022; [7] 2022; [8] 2022; [9] 2020; [10] 2021; [11] 2020 – non-energy uses are not included; [12] 2020; [13] 2020; [14] future investments needed in renewables in end uses, district heating, biofuels and bio-based innovative fuels; [15] 2022; [16] Recent years value is an average between 2010 and 2020; [17] future investments in energy conservation and efficiency include those in bio-based plastics and organic materials, chemical and mechanical recycling and energy recovery; [18] 2021; [19] 2020; [20] 2022; [21] 2022; [22] 2022; [23] 2021; [24] the share for green hydrogen is 40% in 2030; [25] the share for green hydrogen is 94% in 2050; [26] 2022; [27] future investments needed in electrolysers, infrastructure, H2 stations, bunkering facilities and long-term storage; [28] 2022; [29] Includes CO₂ capture in natural gas processing, hydrogen, other fuel supply, power and heat, industry, direct air capture of facilities in operation, 2022; [30] Current total capture corresponds to fuel supply, 2022; [31] 2022. CCS/U = carbon capture and storage/use; BECCS = bioenergy, carbon capture and storage; EV = electric vehicle; RE = renewable energy; yr = year; m2 = square metre; EJ = exajoule; Gt = gigatonne.

The share of renewable energy in the global energy mix would increase from 16% in 2020 to 77% by 2050 in IRENA’s 1.5°C scenario. Total primary energy supply would remain stable due to increased energy efficiency and growth of renewables. Renewables would increase across all end-use sectors, while a high rate of electrification in sectors such as transport and buildings would require a twelve-fold increase in renewable electricity capacity by 2050, compared to 2020 levels. Globally, annual renewable power capacity additions would need to reach an average of 1 066 GW per year from 2023 to 2050 under the 1.5°C scenario.

Electricity would become the main energy carrier, accounting for over 50% of total final energy consumption by 2050 in the 1.5°C scenario. Renewable energy deployment, improvements in energy efficiency and the electrification of end-use sectors would contribute to this shift. In addition, modern biomass and hydrogen would both play more significant roles, meeting 16% and 14% of total final energy consumption by 2050, respectively.

By 2050, 94% of hydrogen would be renewables-based in the 1.5°C scenario. Hydrogen would play a key role in the decarbonisation of end-uses and flexibility of the power system. The 1.5°C Scenario envisages that total final energy consumption would decrease by 6% between 2020 and 2050, due to efficiency improvements, deployment of renewables, and changes in behaviour and consumption patterns.

An enduring investment gap

A cumulative USD 150 trillion is required to realise the 1.5°C target by 2050, averaging over USD 5 trillion in annual terms. Although global investment across all energy transition technologies reached a record high of USD 1.3 trillion in 2022, annual investment must more than quadruple to remain on the 1.5°C pathway. Compared with the Planned Energy Scenario – under which a cumulative investment of USD 103 trillion is required – an additional USD 47 trillion in cumulative investment is required by 2050 to remain on the 1.5°C pathway. Around USD 1 trillion of annual investments in fossil fuel-based technologies currently envisaged in the Planned Energy Scenario must therefore be redirected towards energy transition technologies and infrastructure.

Renewable energy investment remains concentrated in a limited number of countries and focused on only a few technologies. Investment in renewable energy (including both power and end-uses) reached USD 0.5 trillion in 2022 (IRENA and CPI, 2023); however, this is around one-third of the average investment needed each year in renewables under the 1.5°C Scenario. Furthermore, 85% of global renewable energy investment benefitted less than 50% of the world’s population and Africa accounted for only 1% of additional capacity in 2022 (IRENA, 2023a; IRENA and CPI, 2023). Investments in off-grid renewable energy solutions in 2021 amounted to USD 0.5 billion (IRENA and CPI, 2023) – far below the USD 15 billion needed annually to 2030. While many technology choices exist, most investments were in solar PV and wind power, with 95% channelled toward these technologies (IRENA and CPI, 2023). Greater volumes of funding need to flow to other energy transition technologies such as biofuels, hydropower and geothermal energy, as well as to sectors beyond power that have lower shares of renewables in total final energy consumption (e.g. heating and transport).

Some 75% of global investment in renewables from 2013 to 2020 came from the private sector. However, private capital tends to flow to the technologies and countries with the least associated risks, be they real or perceived. In 2020, 83% of commitments in solar PV came from private finance, whereas geothermal and hydropower relied primarily on public finance – only 32% and 3% of investments in these technologies, respectively, came from private investors in 2020 (IRENA and CPI, 2023). Stronger public sector intervention is required to channel investments towards countries and technologies in a more equitable way.

Public finance and policy should crowd in private capital, but greater geographical and technological diversity of investment requires targeted and scaled-up public contributions. For many years, policy has focused on mobilising private capital. Public funding is urgently needed to invest in basic energy infrastructure in the developing world, as well as to drive deployment in less mature technologies (especially in end uses such as heating and transport, or synthetic fuel production) and in areas where private investors seldom venture. Otherwise, the gap in investment between the Global North and the Global South could continue to widen.

Overcoming barriers to the transition

Policy makers need to strike the right balance between reactive measures and proactive energy transition strategies that promote a more resilient, inclusive and climate-safe system. Several of the root causes of current crises stem from the fossil fuel-based energy system, such as overdependence on a limited number of fuel exporters, inefficient and wasteful energy production and consumption, and the lack of accounting for negative environmental and social impacts. An energy transition based on renewables can reduce or eliminate many of these. It is therefore the speed of the change that will determine the levels of energy security and economic and social resilience at the national level and offer new opportunities for improved human welfare globally.

Accelerating progress worldwide requires a shift away from structures and systems built for the fossil fuel era. The energy transition can be a tool with which to proactively shape a more equal and inclusive world. This means overcoming existing barriers across infrastructure, policy, workforces and institutions that hamper progress and impede inclusivity (Figure S2).

More can be done in the short term. While the energy transition undoubtedly requires time, there is significant potential to implement many of the available technology options today. Upward trends in the deployment of these solutions demonstrate that the technical and economic case is sound. However, comprehensive policies are needed across all sectors to ramp up deployment, as well as to instigate the systemic and structural overhaul required to realise climate and development objectives.

FIGURE S1 Key energy transition barriers and solutions

A profound and systemic transformation of the global energy system must occur within 30 years

The Global Stocktake at the 2023 United Nations Climate Change Conference (COP28) must serve as a catalyst for scaling up action in the years to 2030 to implement existing energy transition options. Whilst planning must provide room for innovation and additional policy action, a significant scale up of existing solutions is paramount. For example, advancing efficiency and electrification based on renewables is a cost-effective avenue for the power sector, as well as for transport and buildings. Clean hydrogen and its derivatives, and sustainable biomass solutions, also offer various solutions for end uses.

The period following COP28 will be pivotal for efforts to curb climate change and achieve the sustainable development goals outlined in the 2030 Agenda. The energy transition is crucial for delivering on economic, social and environmental priorities. It is imperative for governments, financial institutions and the private sector to urgently re-evaluate their aspirations, strategies and implementation plans to realign the energy transition with its intended trajectory.

Developing structures for a renewables-based energy system

A profound and systemic transformation of the global energy system must be achieved within 30 years. This condensed timeframe necessitates a strategic shift that expands beyond the focus on decarbonisation of energy supply and energy consumption, toward designing an energy system that not only reduces carbon emissions but also supports a resilient and inclusive global economy. As a result, planning needs to extend beyond borders and the narrow confines of fuels to focus on the requirements of the new energy system and the economies it will sustain.

Focusing on the enablers of a renewables-dominated system can help address the structural barriers that hinder progress in the energy transition. Pursuing fuel and sectoral mitigation measures is necessary, but is insufficient to transition to an energy system fit for the dominance of renewables. From energy production and transportation to processing coal, oil and gas, the global infrastructure dedicated to energy will need to change. This will have impacts on power generation, industrial production and manufacturing, as well as on rail, pipelines, shipyards and other means of supplying fossil fuels. Enhancing the focus on systems design will help accelerate the development of a new energy infrastructure and sustain its implementation.

Governments can proactively shape a renewables-based energy system, overcome the flaws and inefficiencies of current structures, and more effectively influence outcomes. The simultaneous, proactive shaping of physical, policy and institutional structures will be essential to realising development and climate objectives, and achieving a more resilient and equitable world. These underpinnings should form the pillars of a structure that supports the energy transition:

Physical infrastructure upgrades, modernisation and expansion will increase resilience and build flexibility for a diversified and interconnected energy system. Transmission and distribution will need to accommodate both the highly localised, decentralised nature of many renewable fuels, as well as different trade routes. Planning for interconnectors to enable electricity trade, and shipping routes for hydrogen and derivatives, must consider vastly different global dynamics and proactively link countries to promote the diversification and resilience of energy systems. Storage solutions will need to be widespread and designed with geo-economic impacts in mind. Public acceptance is also critical for any large-scale undertaking and can be secured through project transparency and opportunities for communities to voice their perspectives.

Policy and regulatory enablers must systematically prioritise the acceleration of the energy transition and a reduction in the role of fossil fuels. Today, the underlying policy and regulatory systems remain shaped around fossil fuels. While it is inevitable that fossil fuels will remain in the energy mix for some time, their share must dramatically decrease as we approach mid-century. Policy frameworks and markets should therefore focus on accelerating the transition and provide the essential underpinnings for a resilient and inclusive system.

A well-skilled workforce is a lynchpin of a successful energy transition. Work by IRENA and the International Labour Organization (ILO) has shown that the renewable energy sector employed some 12.7 million people worldwide in 2022, growing from about 7.3 million in 2012. Energy transition modelling indicates that tens of millions of additional jobs will likely be created in the coming decades as investments grow and installed capacities expand. A broad range of occupational profiles will be needed. Filling these jobs will require concerted action in education and skills building, and governments have a critical role in coordinating efforts to align the offerings of the education sector with projected industry needs – whether in the form of vocational training or university courses. To attract talent to the sector, it is crucial that jobs are decent, and that women, youth and minorities have equal access to job training, hiring networks and career opportunities.

The way forward: Prioritising bold and transformative actions

Achieving the necessary course-correction in the energy transition will require bold, transformative measures that reflect the urgency of the present situation. A considerable scale-up of renewables needs to go hand-in-hand with investments in enabling infrastructure. Comprehensive policies are needed not only to facilitate deployment but also to ensure the transition has broad socio-economic benefits.

Net-zero commitments must be embedded in legislation and translated into implementation plans that are adequately resourced. Without this crucial step, climate announcements remain aspirational, and the necessary progress out of reach. The current energy system is deeply woven into socio-economic structures that have evolved over centuries. This means significant structural change must occur in a condensed timeframe of less than three decades to successfully deliver on the goals of the Paris Agreement.

Every investment and planning decision concerning energy infrastructure today should consider the structure and geography of the low-carbon economy of the future. Energy infrastructure is long-lived, so investment in fixed infrastructure should consider the long term. Electrification of end uses will reshape demand. Renewable power will require existing infrastructure to be modernised, with grid reinforcement and expansion on both land and sea. Green hydrogen production will also occur in locations other than today’s oil and gas fields. The technical challenges and economic costs of redesigning infrastructure should be accounted for, and the environmental and social aspects adequately addressed from the outset.

A just and inclusive energy transition will help to overcome deep disparities that affect the quality of life of hundreds of millions of people. Energy transition policies must be aligned with broader systemic changes that aim to safeguard human well-being, advance equity among countries and communities, and bring the global economy in line with climate, broader environmental and resource constraints.

Supporting developing countries to accelerate the energy transition could improve energy security while preventing the global decarbonisation divide from widening. A diverse energy market would reduce supply chain risks, improve energy security and ensure local value creation for commodity producers. Access to technology, training, capacity building and affordable finance will be vital to unlock the full potential of countries’ contributions to the global energy transition, especially for those rich in renewables and related resources.

Human welfare and security must remain at the heart of the energy transition. Systemic changes beyond the energy sector will be needed to overcome pervasive problems related to human welfare and security, as well as deeply embedded inequalities; a renewables-based energy transition can help alleviate some of the conditions that underly these issues. The more the energy transition can help solve these broad challenges, the more its popular acceptance and legitimacy will rise, provided also that community needs and interests are well represented and integrated into transition planning.

Rewriting international co-operation

The dynamism of energy sectors and geopolitical developments necessitates greater scrutiny of international co-operation modalities, instruments and approaches to ensure their relevance, impact and agility. To achieve a successful energy transition, international co-operation needs to be enhanced and redesigned. The centrality of energy to the global development and climate agenda is undisputed, and international co-operation in energy has increased exponentially in recent years. This co-operation plays a decisive role in determining the outcomes of the energy transition and is a critical avenue for achieving greater resilience, inclusion and equality.

The expanding variety of actors engaged in the energy transition requires an assessment of roles to leverage respective strengths and efficiently allocate limited public resources. The imperatives of development and climate action, coupled with changing energy supply and demand dynamics, require coherence and alignment around priority actions. For instance, investment in systems for cross-border and global trade of energy commodities will require international co-operation on an unprecedented scale. It is, therefore, essential to reconsider the roles and responsibilities of national and regional entities, international organisations, and international financial institutions and multilateral development banks to ensure their optimal contribution to the energy transition.

Achieving the energy transition will require collective efforts to channel funds to the Global South. In 2020, multilateral and bilateral development finance institutions (DFIs) provided less than 3% of total renewable energy investments. Going forward, they need to direct more funds, at better terms, towards large-scale energy transition projects. Moreover, financing from DFIs was provided mainly through debt financing at market rates (requiring repayment with interest rates charged at market value) while grants and concessional loans amounted to just 1% of total renewable energy finance (IRENA and CPI, 2023). These institutions are uniquely placed to support large-scale and cross-border projects that can make a notable difference in accelerating the global energy transition.

Introduction

The year since the publication of the 2022 edition of the World Energy Transitions Outlook has been a challenging one for decision makers. With the world still reeling from the economic effects of the pandemic, the consequences of events in Ukraine escalated what has become one of the worst energy crises in decades. At the same time, the scale of the global climate emergency has become ever more obvious. Unprecedented heat waves in Europe, widespread flooding in Pakistan and the worst drought on record in the Horn of Africa are just a few of the recent extreme weather events that have been linked to climate change. The Intergovernmental Panel on Climate Change (IPCC), in a synthesis report published in March 2023, stressed the need for rapid and far-reaching transitions across all sectors and systems (IPCC, 2023).

As the International Renewable Energy Agency (IRENA) has urged in previous editions of the World Energy Transitions Outlook, a set of complementary transitions – in renewables-based electrification, energy efficiency, and direct uses of renewables in transport, industry and buildings – offer a pathway to the IPCC’s 1.5°C climate target based on technologies and measures that are, for the most part, already available. The past year has demonstrated the clear benefits of this renewables-based pathway in strengthening energy security, reducing the negative effects of fossil fuel price volatility, and making energy more affordable. Renewables have become increasingly competitive relative to fossil fuels in many cases, offering the potential to hold down energy costs while allowing countries to reduce their dependence on imports.

The impacts of the global energy-related challenges countries have faced over the past year – such as rising energy prices, inflation, higher capital costs and energy insecurity – would have been less severe if countries had invested earlier in transition technologies and associated infrastructure in the power and heat sectors. Further delays will compound these challenges. Nonetheless, it is not too late to change course.

Several energy transition indicators show that despite the crisis, there is resilience in the various components of the energy transition, with some even picking up speed. Overall, however, the energy transition is not on track; each year the gap grows between what is being done and what is required. Too many decision makers have been addressing the energy crisis in ways that are incompatible with the longer-term need for profound transformation, not only of the energy sector but of the economy and society as well. The slow pace of progress now will increase investment needs in the future, both to produce the energy we need and to cope with worsening climate change effects. The simultaneous, proactive reshaping of physical, policy and institutional structures will be essential to the realisation of a more resilient, productive and equitable world.

This first volume of the World Energy Transitions Outlook 2023 proposes a 1.5°C-compatible pathway to 2050, while documenting the progress achieved to date in the deployment of investment and energy transition solutions. It presents ways to deal with the short-term energy crisis while remaining on the energy transition path; contains new analysis and information; provides perspectives on the latest developments and progress in energy scenarios and investments; and offers new views on enabling finance and frameworks. The second volume of the outlook, to be published later in 2023, will examine the socio-economic impacts of the energy transition.

2023 Volume 1

This volume comprises three chapters:

- Chapter 1 presents transition pathways to 2030 and 2050 under the Planned Energy Scenario and the 1.5°C Scenario, examining the required technological choices and emission mitigation measures to achieve the 1.5°C Paris climate goal. In addition to the global perspective, the chapter presents transition pathways at the G20 level, and emphasises the G20’s role in reducing emissions and accelerating the deployment of low-carbon technologies. Along with the latest information on the Nationally Determined Contributions from the 2022 United Nations Climate Change Conference (COP27), the emissions gap to the 1.5°C target is discussed. Additionally, it includes an examination of responses to the current energy crisis and their implications for the energy transitions. The chapter concludes with recommendations for policy actions to respond to the present energy crisis and longer-term climate goals.

- Chapter 2 provides sector- and technology-specific details of the transition to 2030 and 2050. The analysis shows that a range of technologies and strategies must be deployed. Renewables must play a dominant role in all end-use sectors, notably electricity, green hydrogen and synthetic fuels produced from renewable power. Bioenergy and biomass feedstocks must also play a growing role, especially in industry and transport. Institutional and regulatory frameworks and policies to propel the energy transition are examined for the power sector, supplies of emerging fuels and end-use sectors.

- Chapter 3 identifies the investments required by 2030 and 2050 under the 1.5°C Scenario, comparing them with current levels. After exploring how governments can balance short- and long-term energy transition investment needs, the chapter examines the pressing need to accelerate investment in infrastructure. Recent trends in energy-transition investment are analysed by technology, region and source of funding. To achieve both an overall scale-up of deployment and a truly global energy transition, public finance (both national and international), co-ordinated regulation, and policy support will play crucial roles in the deployment of renewable energy, especially in regions and countries that have not been able to attract private capital.

Understanding the socio-economic consequences of the transition pathways (at different levels of ambition) is a fundamental aspect of proper planning and policy making. Policy makers need to know how their choices will affect people’s well-being and overall welfare, just as they need to be aware of the potential gaps and hurdles that could affect progress. For the energy transition to yield its full benefits, countries will require a comprehensive policy framework that not only transforms energy systems, but also protects people, livelihoods and jobs.

The climate policy baskets that underlie IRENA’s macroeconometric model, the results of which will be presented in the forthcoming second volume of the World Energy Transitions Outlook 2023, contain a range of measures (e.g. investments in public infrastructure, increased social spending, and cross-sectoral carbon pricing and subsidies) to support a just and inclusive transition, in addition to policies that deploy, integrate and promote energy transition technologies.